NEW SCHEDULE AN APPOITMENT LINK HERE!

425-802-2783 or wahealth@heffins.com

Achieve Alpha Insurance is now Heffernan Insurance Brokers

Recently we are now part of a larger insurance agency, yet all off us are still here to help you with your Individual Health & Medicare needs. The phone number is the same yet our emails all forward to our new ones at Heffernan. You can still email us on the old Achieve Alpha Insurance ones and they forward to us instantly.

Insurance Made Easy!

We Shop for you.

With Achieve Alpha is on your side we help you shop for the best insurance for the price and your needs. Our experts learn about your needs, recommend the right coverages, and find the best options for you by shopping across our large network of health, life, disability and long term care insurance companies. We’ll earn your trust, because we work for you!

Get a Free Quote

Health Insurance

Confused by health insurance enrollment periods, regulations, or even just the state exchange website? You aren’t alone. We can help you get the right plan for your needs and your budget.

Life Insurance

We can help you shop around for the best life insurance policy for your needs. Our goal is to help you get the most affordable policy for what your family or business situation is.

Medicare Insurance

When you turn 65 years old you need to get Medicare coverage. We can help you walk through your options and do a Medicare 101 overview. Reach out to us and will help you or a family member.

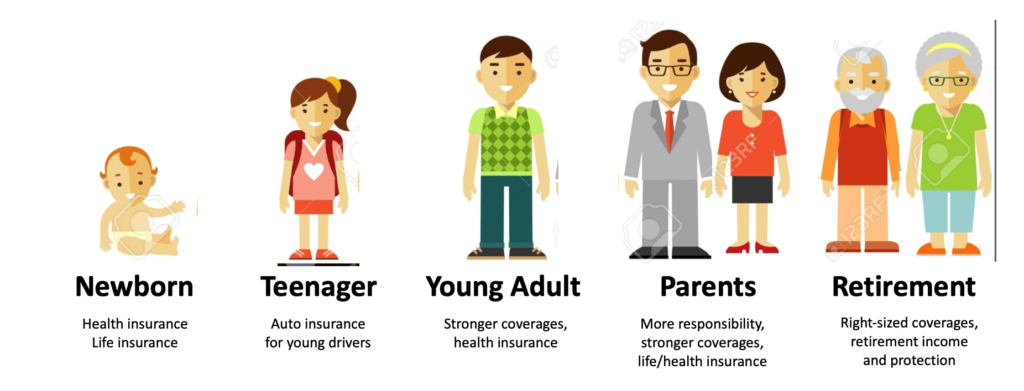

Insurance for All Phases of Life

Insurance for All Phases of Life

Newborn

We can help your newborn get health insurance on the WA HealthPlanFinder. Can also get a low cost life insurance policy that will last their entire life.

Teenager

Turning 16 and getting your drivers license? Auto Insurance is going to be expensive, yet we will help you get the best policy and help coach your new driver.

Young Adult

New responsibilities, need better Auto coverage, a cheap term life policy and learning how insurance works as you start a family. We are here for you!

Adult with Family

Getting all your comprehensive insurance needs with one agency is key. We can help you get coverage that is as affordable as possible for auto, home, life and health insurance. We can help you bundle coverage and get an umbrella policy. Life is complex, lets get your insurance set up right for your entire family needs.

Retirement

We are here to help you retire in style, whether that is getting medicare when you turn 65, auto, home or a permanent life insurance policy that has conservative growth goals. We can help ensure you are covered as you retire and right size your insurance needs and help your retirement income grow and pay out tax free.

Experienced Agents You Can Trust

Achieve Alpha Insurance agents have earned the highest customer satisfaction ratings because we care. We live and work in Washington State. We care about our reputation and our customers; it means everything to us! Local agents who share the same passions as you means we’re around town just like you. We might even meet in passing at the grocery store.

We’ve also been doing this a long time and those years of experience help us determine the right amount of coverage needed for each person based on their individual situations. Coverages’ are not all the same. Insurance policies and insurance companies vary greatly. Which is right for you?

1,800+

Policy Holders

2008

Opened Our Business

50+

5 star reviews

Free Quote

Find out what a tailored insurance plan feels like

Don’t Be Caught Off Guard

Life can throw a lot of nasty surprises at us, and the right protection can help you recover from them. You never know when you’re going to use insurance, of course—but that’s exactly why you need it now. See below for how we can help.

Our Customers Loves Us! Check our References on Yelp

Suzy V.

Aaron S.